Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

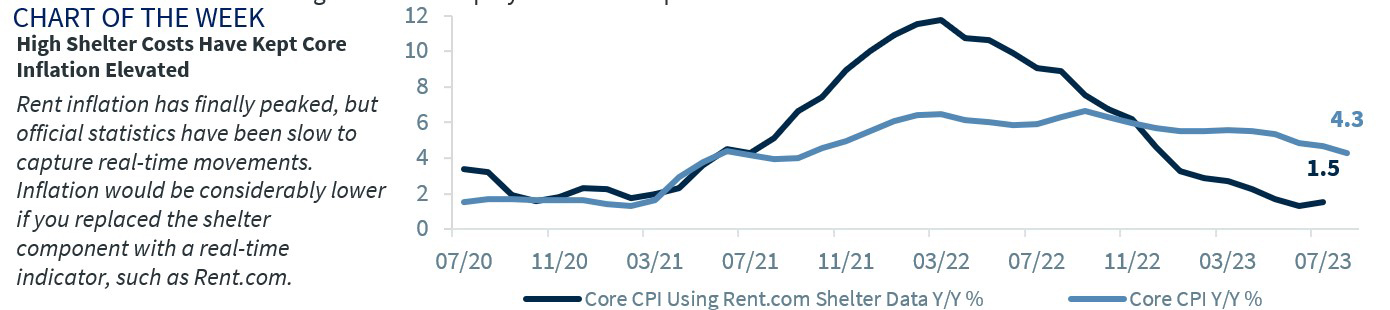

The Energizer Bunny! That’s the term that best describes the U.S. economy. Despite calls for a recession, growth has defied expectations – remaining remarkably resilient thus far this year. While the headwinds to growth (i.e., depleted excess savings, student loan repayments, softening job growth) are building, the economy remains on track for a strong 3Q (Atlanta Fed Q3 GDPNow growth estimate: 4.9%). The latest surge appears to be due to a last burst of pent-up travel demand and soaring manufacturing investment (courtesy of prior stimulus acts). While inflation has eased, the uptick in oil prices (if sustained) could create challenges for the outlook. How will these dynamics shape the Fed’s thinking at the September 19-20 FOMC meeting and impact its updated economic projections? Here are our latest thoughts.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.